CHIEF EXECUTIVE’S REVIEW

The loss of 65 production days at the company’s only revenue-generating asset, the Zondereinde mine, and the effect these losses have had on production and in turn on earnings has clouded the overall performance of the company in 2011.

The Zondereinde mine’s performance has been of concern and it has overshadowed some of the more positive developments in the group, which have been critical steps in realising our longer term strategy of geographic diversification, and adding shallower ounces to our production profile:

- The group’s acquisition of the entire issued share capital of former major shareholder Mvelaphanda Resources Limited (Mvela Resources) through a scheme of arrangement. This follows the protracted unbundling process of Mvela Resources, and gave us access to a cash injection of some R650 million, a critical development for the financing of the development of Booysendal

- The proposed sale of 31.3Moz of the mineral rights pertaining to southern Booysendal to Aquarius Platinum South Africa (Proprietary) Limited (AQPSA) for R1.2 billion thereby enabling us to secure additional funding for Booysendal

- Progress at Booysendal has been satisfactory, and follows on from the approval of the new order mining licence for the Booysendal extension granted in October 2010 in terms of the section 102 amendment; and the issue of the water use licence in May 2011. Construction and development is now a priority, and Booysendal remains on track for first production in early 2013.

PGM markets

Following the economic uncertainties of 2009 the latter months of 2010 and the opening months of 2011 were typified by widespread economic recovery, a recovery realised in most of the principal applications and regions of consumption for Northam’s basket of metals.

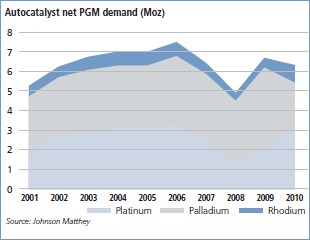

The autocatalyst sector in particular performed strongly throughout this period. In 2010 gross world demand for platinum from the sector increased by more than 40% to reach a total of approximately 3.1Moz out of total demand of 7.8Moz.

Palladium also benefited from autocatalyst demand, which escalated by some 35% to a total of 5.4Moz for the year. For rhodium consumption totaled 725 000oz marking a year-on-year increase of 17%.

In Europe the strong rebound in vehicle sales was underpinned by two principal features:

- firstly, the increased production of diesel-fuelled vehicles – a trend particularly benefiting platinum as the diesel market now accounts for some 50% of European auto-sales; and

- secondly, in Europe the full implementation of the Euro 5 emissions legislation in the heavy duty sector prompted heavier loadings of PGMs in oxidation catalysts and particulate filters on these vehicles.

China’s motor industry maintains its status as the world’s largest producer of vehicles, the majority of which are gasoline fuelled. Chinese autocatalyst demand alone accounts for almost 1Moz of palladium per annum.

In Japan, the motor industry has recovered well from the tragic tsunami earlier this year. In fact, only six months after this disaster, projections for 2011 vehicle production are already encouraging. Although the immediate devastation wrought by the tsunami and the associated nuclear threat in Japan appeared to be localised, the courage of the Japanese people in the midst of this disaster was humbling to say the least; with the exception of some minor rescheduling of shipments for logistical reasons, our customers and the ‘receivers’ of metal operated largely on a business as usual basis – a truly commendable effort.

Retail sales of jewellery contracted sharply throughout the course of 2010 as a result of the strong upward movement in the platinum price – a trend that continued into 2011. Thus gross demand for platinum from the jewellery sector shrank to some 2.4Moz during 2010 – a contraction of 15% on the prior year. Jewellery demand for palladium trended similarly – diminishing by 20% to 620 000oz for the year.

And as the average platinum price for the first six months of 2011 increased towards $1 800/oz, so the upward trend in prices, along with significant price volatility over this period, conspired to reinforce the challenges facing manufacturers and retailers in this sector.

In the industrial sector demand for PGMs grew by almost 50% across the course of 2010 – a trend supported by surging demand for metal from each of the chemicals, glass products and electrical sectors in both established and newly emerging markets. Gross industrial demand for platinum was 1.7Moz in 2010 and 2.5Moz for palladium.

The chemical sector also manifested growing demand for platinum particularly in India and China where investment in new production capacity has driven demand for the platinum-based chemical catalysts. And in the glass and electrical sector once again, rampant demand has endured for the broad range of goods and components required by household consumers and commercial and industrial buyers alike.

Platinum’s appeal in the investment sector was mixed – holdings of metal in platinum ETFs saw growth in US held funds but profit taking in the European based funds. ETF demand for palladium surged across the course of 2010 but has since shown signs of softening. Nevertheless total ETF holdings continue to account for significant volumes of metal and currently stand at approximately 1.5Moz in platinum and 2.1Moz in palladium.

Performance

Given the growing fundamental demand for our basket of metals, dollar prices were well supported; in rand terms too the average rand basket price received was 12.4% higher year on year, peaking at R366 393/kg in February 2011, and averaging R323 899/kg for the year. Sadly, this failed to translate into better revenues, given the slump in production volumes during the year. A total of 65 production days were lost at Zondereinde, owing to strike action in the first half of the year, and safety stoppages spread throughout the year.

With the relatively high fixed cost base performance is critically linked to volumes at the Zondereinde mine – so the volume shortfalls translated into significantly lower revenues, and consequently lower profits, earnings and dividends, and helped to drive cash costs up by 29.3% to R279 118/kg.

On one level the performance at Zondereinde over the year should not have come as a surprise to the market. Management has warned of the difficulties in accessing the Merensky reef horizon, the pressure of having lost ore reserve availability associated with the sterilisation of the eastern part of the mine, and the ongoing difficulties and delays associated with establishing mining face in the north-west quadrant. This situation was always going to pose challenges to the production position at Zondereinde which was then further bedeviled by an unprecedented six-week strike in the first half of the year, and a number of accidents which in turn led to a series of safety stoppages, contributing to a 22.2% decline in production volumes – Zondereinde’s worst performance in more than a decade.

Although earnings were 45.9% lower year on year, we did declare dividends, albeit at a lower level, in both halves of the year. Internally we have given a lot of consideration to the company’s ability and volition to pay dividends, and what signals the non-payment of dividends would send to our shareholders. This is particularly important since the unbundling of Mvela Resources and our exposure to a much larger offshore base of shareholders, many of whom have certain investment mandates in place which rely on the receipt of dividends from their investments. That Northam, as a relatively small producer, with only one revenuegenerating asset remains in a position to reward shareholders, however modestly, should provide some comfort and reassurance to shareholders. We have always paid excess cash to shareholders, and that is something we will continue to do, hopefully at higher levels, as we recover from the operating difficulties at Zondereinde, and as we start to benefit from the cash flows at Booysendal.

We have provided more detail on the operating and financial performance of Zondereinde in the financial and operating reviews elsewhere in this report. The recovery at Zondereinde is critically associated with the availability of Merensky reef. Although it will be some 18 months before we are out of the woods, F2013 should see some gradual increase in the build-up of volumes from the establishment of face on the western side of the mine, and the extraction of tonnages from the deepening project, where we should also see an incremental improvement in productivity and efficiencies given the proximity to the shaft and the transport infrastructure being put in place.

Progress at Booysendal has been satisfactory, with infrastructural and construction activities continuing apace. Mining activites, although a little slower than we would have liked, owing to some minor initial challenges, will pick up in the year ahead. A particularly pleasing development over the year has been the permits and approvals we have received in order to fast track the mining, and get the concentrator built on site. We remain on track to commission the concentrator in the second half of the 2013 financial year, building up to full production during 2014. Some changes of scope in the tailings dam along with other minor adjustments, have contributed to the capex profile of this project increasing to R3.9 billion, from a March 2010 base cost of R3.6 billion. In the broader context of establishing a mine and infrastructure in this area, we don’t believe this is a significant variance, and the modifications it does provide will stand us in good stead when we begin to apply our minds to building the next phase of the Booysendal mine.

We have kept shareholders informed of various corporate activities over the year. These have been useful developments which have served to boost our internal cash reserves. Although the timing of the unbundling of Mvela Resources was largely out of our hands, the cash injection emanating from that transaction, along with the proposed sale of the Booysendal South mineral rights to AQPSA has been timeous in resolving our near-term funding requirements. We are confident that we will be in a position to continue funding Booysendal from, amongst others, internal retentions and a revolving credit facility of R1 billion which is currently being finalised.

Rebalancing reserves and resources

In attempting to provide the market with additional information, in the interests of improved disclosure and transparency, our ore resource and reserve statement this year includes for the first time an inferred resource for the Middeldrift section of the Zondereinde mineral right area. It also includes the PGM resources attributable to the company from the Dwaalkop and Pandora joint ventures. The Booysendal resource classification includes a table showing the resources for southern Booysendal which are the subject of the transaction with AQPSA. Please see the mineral reserve and resource statement (PDF - 432KB).

Integrated reporting and King III

Northam is fully committed to timeous, relevant and transparent communication of issues relevant to all stakeholders, and has adopted an integrated approach to reporting and the guidance provided by King III.

During the year the board commissioned a King III gap analysis by Ernst & Young Inc. A number of areas have been identified for improvement. Management is currently putting action plans in place to deal with these matters.

Good progress has been made with the implementation of systems to integrate sustainability data into the broad reporting framework. We once again undertook an assessment of the material sustainability issues both from the group’s and stakeholders’ perspectives. Critical amongst these are:

Operating the Zondereinde mine and its concentrating and smelting operations efficiently and cost-effectively.

More detail on the way in which the group is undertaking this may be found in the operational review of Zondereinde.

Ensuring the safety of employees and contractors.

Over the past ten years safety at Zondereinde has shown a steadily improving trend. It is with sadness therefore that the company advises that there were five fatalities during the year. Investigations into the causes of these accidents have been undertaken in close co-operation with unions and the DMR. An intensive safety campaign has been launched to reverse the recent disappointing performance.

Establishing and maintaining constructive relations with unions.

Industrial relations have again been challenging. A total of 37 days were lost during the year owing to industrial action at Zondereinde. A concerted effort has since been launched to improve communication and relationships.

Achieving legislative and regulatory compliance.

The Zondereinde mine’s new order mining rights are now in place, having applied for conversion of its old order mining rights in 2006. Zondereinde has an exemption to operate without a water use licence, which was applied for in June 2005. All mining rights and permits have been awarded to the Booysendal project following the allocation of its water use licence on 17 May 2011.

Delivering the Booysendal project at an acceptable cost of capital, to turn to account its extensive resources for a broad range of stakeholders.

A detailed account of the progress made at the Booysendal project is discussed under the operational review.

Implementing the ISO14001 environmental management system and to achieve certification against this standard.

The Zondereinde mining operation was awarded ISO14001 certification on 28 February 2011. Application for this standard and certification of Zondereinde’s metallurgical complex is underway. The ISO14001 standard will also be implemented at Booysendal.

Optimising water usage both at Zondereinde and at Booysendal.

Water is fundamentally important for Zondereinde mine, not just from an environmental and permitting perspective, but also because the mine uses water as its primary source of energy for underground operations through a shaft-based hydropower system. Zondereinde’s operations do not source water through abstraction, and the division aims to achieve zero discharge into the surrounding environment.

At Booysendal, water allocation too, is of critical importance.

Northam has considered the risks and opportunities relating to water availability in its voluntary submission to the Carbon Disclosure Project (CDP) Water Disclosure for the second consecutive year. Download the CDP Water Disclosure 2011 Global Report.

Optimising energy consumption and investigating potential and cost-effective alternative sources of energy.

At Zondereinde, electricity accounts for 10.4% of total operating costs. This is expected to increase as Eskom’s rates continue to reflect the NERSA-approved tariff increases. At Booysendal, optimisation studies undertaken during F2010 resulted in a revised mine design and higher rate of production at full capacity, which may result in electricity consumption exceeding the initially allocated 20MVA during peak demand periods. The revised design also makes provision for an energy management system, which is still to be formally approved by Eskom, and the introduction of energy recovery strategies.

To debate, monitor and manage our climate change strategy and, as part of that, to reduce our CO2 emissions.

Climate change presents moderate risks for Northam on a physical an d regulatory front. However, climate change also presents an opportunity as PGMs are used in technologies that bring about reduction in noxious gases. Indeed, the global trend of tightening emissions legislation continues to stimulate PGMs usage in autocatalysis. For more detailed information on greenhouse gasses (GHGs) and Northam’s assessment of the risks and opportunities presented to the company as a result of climate change, view Northam’s submission to the Carbon Disclosure Project 2011 annual survey which may be found at www.cdproject.net.

To identify conservation priorities in its areas of operation and, where necessary, to work with local authorities and conservation professionals in developing appropriate offsets.

Given that Booysendal is located in a biodiversity-sensitive region, the company has developed a unique and progressive structure that will see oversight of land under management as a distinct and equal role to that of the management of the mine. Further, Booysendal is in the process of establishing an offset trust to be funded during the life of mine, for conservation in perpetuity.

Identifying and engaging with stakeholders on a regular basis, especially community stakeholders.

Stakeholder engagement and relationships are deeply entrenched at the well-established Zondereinde mine. Zondereinde’s Social and Labour Plan (SLP) has been approved by the DMR and work is now underway to implement these in conjunction with the Integrated Development Plans for local communities. Stakeholder identification and engagement at Booysendal is a far more complex undertaking, complicated by the scale, proximity and needs of local communities. A stakeholder engagement action plan is currently being developed and various forums have been set up to deal with concerns from stakeholders and to facilitate the flow of meaningful benefits to communities. A particular issue of concern at Booysendal in recent months has been the allocation of jobs; this is expected to intensify as the project is located in a region with little economic activity. Booysendal’s SLP seeks to address some of the needs in the area, but it will be difficult for a single mining company to have a significant impact.

To attract and retain investors in the company so as to maintain its relative value for shareholders and to be able to raise capital cost-effectively to fund growth.

Over the years the group’s shareholder base has been relatively stable. With the recent unbundling of its major shareholder, Northam has retained its black economic empowerment status, and has acquired a strong new shareholder base, with some 32% now comprising offshore shareholders (June 2010: 17%). The recent global economic turmoil, and the ongoing debate on nationalisation have done little to support resource stocks, and we have seen some largescale sell-offs in the Northam stock, in what appears to be offshore investors losing their appetite for emerging market risk. We don’t believe that this “short-termism” does the market any good, and that the stock should start finding its level once some stability takes hold again in the global economy.

Outlook for 2012

Looking ahead then to the 2012 financial year, we will be watching the market cautiously; despite our view that our basket of metals will remain well supported in the key sectors of offtake, the likelihood of slowing rates of global growth and even the possibility of a return to a recessionary environment cannot be discounted.

In the autocatalyst sector the outlook for further gains in vehicle production and sales remains positive especially so in China, where despite the risk of some economic slowdown car ownership has become clearly entrenched as a key aspiration among large sectors of the Chinese population.

In projecting our future prospects, the performance of the South African currency against the US dollar is obviously a critical area, which we keep a close watch on. We remain conscious of projections that the rand will weaken in the longer term; the rand’s protracted strength over five years now, however, has been confounding. Given the state of the global markets, the debt situation in Europe and the United States, we would expect more volatility going forward and we will need to keep a tight rein on costs, our production profile and those aspects of the business which we have some control over.

Glyn Lewis

Chief executive

30 September 2011

Surface earthworks and the reverse decline boxcut at Booysendal

Convertor at Zondereinde