ECONOMIC PERFORMANCE

Management approach

Based on market capitalisation, Northam is considered to be a mid-tier PGM company. However, unlike many of its peers and smaller producers, Northam is unique in that it has full ownership of its production stream, from mining to processing to marketing.

At Zondereinde, Northam’s smelter complex produces final precious metal concentrate which is processed in terms of a long-term toll-refining contract with Heraeus GmbH (Heraeus). The precious metals emanating from the Heraeus refinery are shipped to Northam’s customers in Europe, Japan and North America. The by-product base metals, copper and nickel sulphate, are extracted at the on-site base metals removal plant and are sold in the domestic market.

Performance F2011

Northam’s integrated annual report for F2011 provides a comprehensive review of the operational and financial performance of the company and the broader material ESG issues that underpin the company’s business performance.

- 37 days were lost during F2011 as a result of industrial action at Zondereinde, resulting in revenue losses of approximately R380 million.

- A total amount of R688 million (F2010: R132.4 million) R307 899/kg was spent on capital expenditure on the new Booysendal mine during the year. Project expenditure is anticipated to peak at R2.2 billion during 2012.

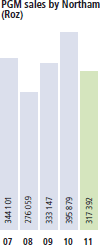

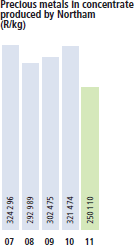

- Metals in concentrate produced by Zondereinde decreased by 22.2% to 7 779kg (F2010: 9 999kg) largely due to the loss of shifts related to industrial action and safety stoppages.

- Unit costs continue to be driven by mining input costs, primarily labour and power, increasing above the rate of inflation, and resulting in a 28.1% increase in operating cost to R279 118/kg (F2010: R279 118/kg) and a 29.3% increase in cash operating costs to R279 118/kg (F2010: R215 900/kg).

- Operating profit was 50.9% lower at R385 million compared to R785 million.

- The average rand price received for Northam’s basket of metals increased from R288 255/kg to R323 899/kg.

- Profit attributable to shareholders decreased by 65% from R641 million to R349.2 million.

- Sales revenue decreased by 9.5% from R 3.9 billion to R3.6 billion owing to lower sales volumes.

- Shareholders received R90 million (F2010: R216 million) by way of dividends.

- Earnings per share decreased by 45.9% to 96.2 cents compared to 177.9 cents in F2010.

| 2011 | 2010 | ||||

|---|---|---|---|---|---|

| Notes in annual financial statements | % | R 000 | % | R 000 | |

| Sales revenue | 23 | 3 571 048 | 3 945 083 | ||

| Less: Purchase of goods and services in order to operate mine and produce refined metal | 24 | (1 984 975) | (1 966 865) | ||

| Value added by operations | 91.6 | 1 586 073 | 91.3 | 1 978 218 | |

| Add: Share of earnings from associate | 26 | 0.4 | 7 248 | 0.6 | 12 440 |

| Investment income | 27 | 4.9 | 85 520 | 7.7 | 167 655 |

| Sundry expenditure/income | 28 | 3.1 | 53 148 | 0.4 | 9 557 |

| Total value added | 100.0 | 1 731 989 | 100.0 | 2 167 870 | |

| Value distributed | |||||

| Employees | 35 | 51.1 | 883 444 | 40.2 | 873 419 |

| Salaries and wages | 49.9 | 863 719 | 39.7 | 861 411 | |

| Contributions to retirement benefit funds | 4.3 | 74 096 | 3.1 | 68 211 | |

| Contributions to health-care funds | 3.2 | 54 606 | 2.1 | 45 079 | |

| Pay-as-you-earn deducted | (6.3) | (108 977) | (4.7) | (101 282) | |

| Government | 19.8 | 342 972 | 21.2 | 462 829 | |

| Mining and non-mining tax including capital gains tax | 29 | 8.3 | 143 048 | 12.1 | 262 934 |

| Deferred tax | 29 | 1.7 | 29 933 | 0.8 | 18 391 |

| State's share of profits | 29 | – | – | 1.4 | 30 660 |

| Secondary tax on companies | 29 | 0.5 | 9 020 | 1.0 | 21 616 |

| Royalties | 3.0 | 51 994 | 1.2 | 27 946 | |

| Pay-as-you-earn deducted from employees | 6.3 | 108 977 | 4.7 | 101 282 | |

| Providers of capital | |||||

| Dividends | 5.2 | 90 202 | 10.0 | 216 158 | |

| Broader community | |||||

| Corporate social investment | 0.2 | 4 116 | 0.6 | 12 140 | |

| Total value distributed | 76.3 | 1 320 734 | 72.2 | 1 564 546 | |

| Retained by company | 23.7 | 411 255 | 27.8 | 603 324 | |

| Depreciation | 25 | 8.4 | 147 838 | 7.7 | 167 346 |

| Decommissioning provision to meet statutory obligations | 24 | 0.3 | 4 410 | 0.5 | 11 110 |

| Retained income | 15.0 | 259 007 | 19.6 | 424 868 | |

| 100.0 | 1 731 989 | 100.0 | 2 167 870 | ||

Direct and indirect economic impacts include:

- Contributions of R13.6 million (F2010: R23.1 million) towards the Employee Empowerment Trust.

- 9 983 employment opportunities (6 738 employees, 1 504 long term contractors and 687 short term contractors at Zondereinde and 1 054 people, mostly construction contractors at Booysendal) directly and indirectly, drawing labour from the area surrounding its operations and other labour sending areas.

- Shareholders received R90 million (F2010: R216 million) by way of dividends.

- R8.8 million spent on township and land development to promote affordable housing and home ownership amongst its employee base. During the year 100 houses were sold to its employees.

- Taxes paid to government at local and national level amounted to R343 million (F2010: R463 million). No significant financial contributions were received from government.

- Corporate social investment amounted to R4.1 million (F2010: R12.1 million).

Black economic empowerment

Northam’s black economic empowerment (BEE) strategy is aimed at broad-based transformation at all levels of the company. Compliance with the Mineral and Petroleum Resources Development Act (MPRDA) and the Broadbased Socio-economic Empowerment Charter (the Mining Charter) is continuously monitored as required by the provisions of the mining licence.

After a protracted process, Northam’s controlling shareholder, Mvelaphanda Resources Limited, unbundled its share in the company during the second half of F2011. The company has retained its black economic empowerment ownership rating, and acquired a strong new shareholder base, with some 32% now comprising offshore shareholders. Although the Toro Employee Empowerment Trust does not have an equity stake in Northam, it receives 4% of Northam’s after tax profits. This interest is regarded as equivalent equity, resulting in Northam’s current BEE shareholding being 26.1%

The Toro Employee Empowerment Trust, which was established in August 2008, represents the interests of some 98.7% of the company’s Zondereinde employees. During F2011 the company contributed R13.6 million (F2010: R23.1 million). In F2011, the net income of the trust was R3.4 million (F2010: R0.3 million). The net interest of the beneficiaries at 30 June 2011 was R85.5 million (F2010: R70.9 million), with the first payouts to employees planned for 2013.

Mining rights and permits

During the year, Zondereinde mine was granted new order mining rights, having applied for conversion of its old order mining rights in 2006. Zondereinde has an exemption to operate without a water use licence, which was applied for in June 2005. All mining rights and permits have been awarded to the Booysendal operation following the allocation of its water use licence on 17 May 2011.

| Applied for | Date of application | Minerals | Status | Zondereinde |

|---|---|---|---|---|

| Old order mining right 8/98 | Conversion | April 2006 | PGE + base metals | Executed |

| Old order mining right 1/2000 | Conversion | April 2006 | PGE + base metals | Executed |

| Booysendal | ||||

| Old order mining right 19/2003 | Conversion | June 2008 | PGE + base metals | Executed and registered |

| Addition of new order prospecting rights 12 and 13/2005 | Section 102 amendment | June 2008 | PGE + base metals | Executed and registered |

| Booysendal extension | Section 102 amendment | August 2010 | PGE + base metals | Executed and registered |

| EMP amendment | ROD | February 2010 | n/a | Approved |

| Water use licence | Water use licence | February 2010 | n/a | Approved |

Economic transformation

Northam is mindful of its role in transforming its procurement base to include emerging entrepreneurs and to provide access to vendors who are HDSAs. The company’s procurement policy therefore gives BEE companies preferred supplier status. This means that BEE companies on Northam’s vendor list are given preference when contracts are awarded provided they are commercially competitive.

Systems to identify HDSA suppliers and to monitor and nurture expenditure with these suppliers, particularly at the operational level, are in place at both Zondereinde mine and the Booysendal mine.

Northam hosts open days for suppliers at both its operations to inform interested parties of the company’s requirements, policies and opportunities.

At Booysendal, Northam completed an exercise of updating the company’s vendor list to include small and medium sized HDSA companies from the surrounding area in order to distribute wealth amongst the local community. Local procurement at Booysendal is discussed further in the community section of this report.

In F2011, Northam’s total procurement amounted to R2.4 billion (F2010: R1.9 billion), of which the total HDSA/BEE procurement component (with BEE equity or BEE ownership of greater than 5%) amounted to R1.6 billion or 65% (F2010: 48% of the total).

In line with the requirements of the Mining Charter, Northam reports BEE/HDSA expenditure at 18.4% (F2010: 10.3%) for capital goods, 35.6% (F2010: 23.5%) for consumables/custom purchases and 10.7% (F2010: 14.2%) for services.

Beneficiation

Northam’s commitment to local beneficiation is demonstrated in the role it has played in facilitating the development of the Heraeus for refining in Port Elizabeth with the DMR and Mintek.

As part of this process, a percentage of Northam’s metal is made available to Heraeus locally for industrial use. Both Northam and Heraeus have articulated a commitment to building local intellectual capital and to this end discussions have been initiated with a number of scientific, research and educational institutions.